India’s MSME sector employs over 34 crore people, making it one of the country’s largest sources of employment. Yet many small business owners still assume that affordable EWA for SMEs in India is a benefit reserved for large enterprises like Infosys or Swiggy. That is no longer the case. Today, earned wage access (EWA) solutions are available for businesses with as few as 10 employees, often at zero cost to the employer.

As competition for skilled talent intensifies and employee expectations evolve, SMEs are looking for practical ways to improve financial wellness, reduce attrition, and strengthen employee engagement; without increasing payroll costs. Earned wage access offers a simple way to achieve all three by allowing employees to access a portion of their already-earned salary before payday.

Read on, we’ll explain what earned wage access actually costs an SME, how the funding model works, and the steps to implement an EWA program in 2026.

Is EWA Affordable for Small Businesses in India?

Yes, for the employer, EWA is free. Modern EWA platforms are funded by RBI-registered NBFC financing partners, not by the business itself. The employer’s cash flow is untouched mid-month; the only party paying a fee is the employee, and that fee is small and optional.

The misconception comes from how older salary-advance processes worked: an HR or finance team manually approving and disbursing advances from company funds. EWA platforms replaced that model. The financing sits with the NBFC partner, not the payroll account.

That reframes the real question for an SME owner. It isn’t whether the business can afford to offer EWA, there’s no employer cost to weigh against the budget. The more useful question is whether the business can afford the attrition, recruitment, and productivity costs of not offering it.

This mindset shows up across sectors, from manufacturing to retail to IT services. For IT MSMEs specifically, we’ve written about how EWA helps smaller tech firms compete with larger employers on benefits.

The 4 SME Myths About EWA — Debunked

If you’ve hesitated on EWA before, it’s probably for one of these four EWA myths presented as problems, and each one is easier to resolve than it looks.

1. “We’d have to fund the advances.” Not with Jify. NBFC partners transfer funds directly to employees; the employer is only involved at month-end payroll deduction.

2. “We’re too small.” Jify works with companies from 10 employees upward. There’s no minimum size that disqualifies a small business.

3. “We don’t have an HRMS.” Jify integrates with platforms like Keka and Greytip, but also supports a simple offline upload for businesses running payroll manually.

4. “It’ll create payroll work.” Accessed amounts are deducted automatically as part of the normal payroll cycle, no manual reconciliation required.

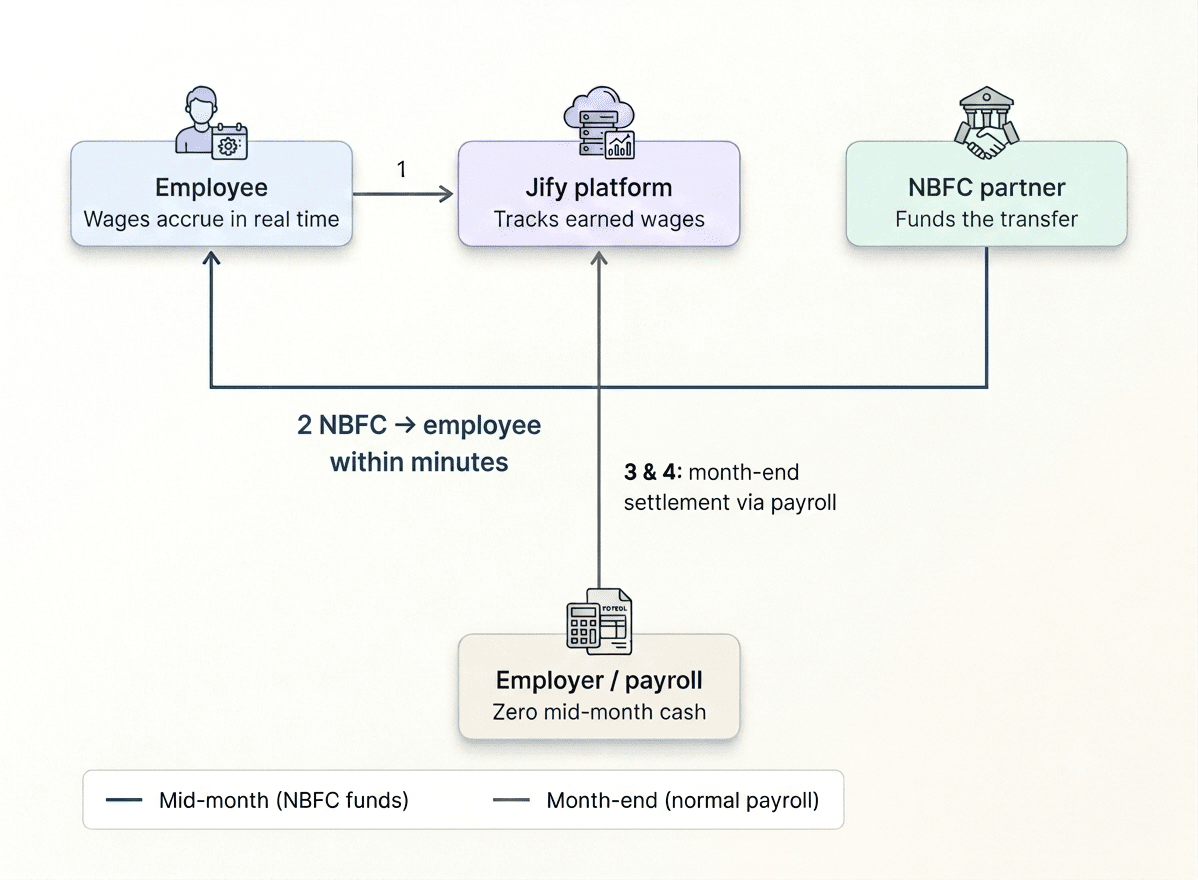

How Does EWA Funding Work If the Employer Doesn’t Pay?

Jify’s NBFC financing partners fund the transfer to the employee directly. The employer only enters the process at month-end, when the accessed amount is deducted from the employee’s payslip as part of the standard payroll run.

The flow has four steps:

- Employee works, wages accrue in the Jify app in real time as the pay cycle progresses.

- Employee requests a portion of earned wages through the app, funds reach their bank account within minutes, paid by Jify’s NBFC partner.

- At month-end, the employer deducts the accessed amount from the employee’s payslip as part of the normal payroll run, no separate process required.

- The employer settles with Jify as part of the regular payroll cycle, with no advance payment required before month-end.

There is no advance payment to Jify required before month-end, no working-capital exposure, and no disruption to the business’s existing cash flow.

What Does EWA Actually Cost an SME? (The Full Breakdown)

EWA through Jify is free for employers. The only cost in the system is a small per-transaction processing fee paid by the employee, starting as low as ₹5. There is no setup fee, no monthly platform fee, and no per-transaction cost charged to the company.

| Cost Component | Employer Cost | Employee Cost |

| Setup / onboarding | ₹0 | — |

| Monthly platform fee | ₹0 | — |

| Per-transaction fee | ₹0 | From ₹5 per withdrawal |

| Payroll system changes | None required | — |

| Dedicated support | ₹0 | — |

| Hidden / recurring costs | None | None |

Get Jify for your business. Free to set up, zero employer cost. Book a demo at jify.co/contact-us

The EWA Cost Comparison: 50-Person vs 200-Person SME

Considering the employer cost is zero, the relevant comparison isn’t EWA cost versus budget; it’s the potential value of reduced attrition against the cost of replacing employees who leave. The scenarios below model a blue-collar workforce earning ₹15,000 to ₹20,000 per month, using industry-standard estimates for frontline replacement cost and attrition rates in India.

Calculation basis:

Replacing a frontline worker in India costs approximately 40% of the annual salary, according to HR industry estimates. Frontline attrition typically ranges between 25% and 35% per year. For a workforce earning ₹15,000 to ₹20,000/month, that puts replacement cost at ₹70,000 to ₹1,00,000 per exit.

| Metric | 50-person SME | 200-person SME |

| Average monthly salary | ₹15,000 – ₹20,000 | ₹15,000 – ₹20,000 |

| Annual salary per employee | ₹1.8 – ₹2.4 lakh | ₹1.8 – ₹2.4 lakh |

| Replacement cost per exit (at 40%) | ₹72,000 – ₹96,000 | ₹72,000 – ₹96,000 |

| Annual attrition (at 30%) | 15 exits/year | 60 exits/year |

| Total annual attrition cost | ~₹12.75 lakh | ~₹51 lakh |

| Saving from a 10% attrition reduction | ~₹1.3 lakh/year | ~₹5.1 lakh/year |

| Saving from a 20% attrition reduction | ~₹2.55 lakh/year | ~₹10.2 lakh/year |

| Employer cost of EWA | ₹0 | ₹0 |

Want to model this for your own company size, salary band, and attrition rate? Try the Jify retention savings calculator– enter your numbers and see the projected savings in under a minute.

What Do SMEs Get When They Sign Up for Jify?

SMEs that sign up for Jify get a full EWA platform with no employer-side cost or payroll disruption. The core feature set includes:

- On-demand salary access for all eligible employees– every worker on the roll, from shop-floor staff to office roles, can access earned wages the moment they need them.

- A rule engine customisable by grade, department, or tenure– the employer decides who can withdraw, how much, and how often, with limits set by role or seniority.

- A real-time dashboard with employee usage analytics– HR sees who’s using EWA, how often, and for what value, without waiting for month-end reports.

- HRMS integration with platforms including Keka, Greytip, Darwinbox, and ZingHR, or offline Excel/CSV upload for companies without one– no forced tech upgrade to onboard.

- Zero change to existing payroll workflows– accessed amounts are deducted automatically, so the payroll team’s process stays untouched.

- A 1–3 day go-live timeline– most SMEs are live and transacting inside a working week.

- A dedicated onboarding team plus a 24/7 helpline– one point of contact for setup, plus round-the-clock support for employees.

- ISO 27001:2013-certified security– enterprise-grade data protection at no extra cost.

- Financial wellness tools for employees, coaching, savings, and rewards at no extra employer cost– a full benefit stack, not just wage access.

EWA in Action — What Indian SMEs Are Saying

Businesses across retail, eyewear, and logistics report faster advance processing and lower admin load after adopting Jify. A few examples from Jify’s case studies:

RS Brothers, a retail business, processed over ₹2 crore in salary advances through Jify at zero administrative cost to the company.

Lenskart cut advance-processing time from roughly 4 days down to about 24 minutes after switching to Jify’s platform.

Porter, a logistics company, used Jify to extend financial wellness support to its delivery workforce without adding cost to its operating budget.

Full details are available in Jify’s case study library.

What Should SMEs Look for When Choosing an EWA Provider?

- Minimum company size supported: some providers won’t take on businesses under 100 or 200 employees. Confirm the provider actively serves companies your size, not just accepts them.

- Who funds the float: if the employer is expected to fund advances from company cash, it isn’t true EWA; it’s a repackaged salary advance with new admin. The provider’s NBFC partner should carry the float.

- Integration options for companies without an HRMS: many SMEs run payroll on spreadsheets. The provider should support offline data uploads, not just API integrations.

- Go-live timeline: days, not weeks. Anything longer suggests the platform wasn’t built for lean onboarding.

- Compliance certifications: ISO 27001, VAPT audits, and NBFC partners registered with the RBI. These aren’t optional for a system that touches employee salary data.

- Support model: a dedicated onboarding team and human helpline, not just a chatbot. SME HR teams don’t have the bandwidth to debug integrations alone.

- Transparency on employee-side fees: the per-transaction fee should be disclosed upfront, in writing, with no hidden interest or subscription components.

- Withdrawal controls: the employer should be able to set limits by tenure, grade, or department, and adjust them without provider involvement.

The Most Affordable Employee Benefit You Haven’t Offered Yet

The most impactful employee benefit isn’t always group health insurance or team lunches, sometimes it’s giving people control over money they’ve already earned.

For an Indian SME, EWA is a rare benefit that costs the employer nothing to offer and comes with a clear operational case: lower attrition risk, less admin load, and a workforce with more financial breathing room.

In a market where blue-collar attrition can hit 35% and every exit costs upwards of ₹70,000, that’s not a soft benefit, it’s a retention lever with a measurable ROI and zero downside.

For a fuller view of what EWA delivers across the Indian workforce, see our complete guide to the benefits of earned wage access in India.

Book a free Jify demo. Go live in under 3 days. Talk to the Jify team.

Frequently Asked Questions for SME Owners

1. Does EWA cost the employer anything?

No. With Jify’s model, the employer pays nothing to offer EWA, no setup fees, no monthly platform fees, and no per-transaction charges for the company. The only fee is a small per-transaction processing charge paid by the employee, starting at ₹5. Jify’s NBFC financing partners fund the wage access, so there’s no working-capital impact on the employer.

2. How small can a company be and still use Jify?

Jify works with companies of 10 employees or more. There’s no minimum employee count that disqualifies a small business, whether you have 15 staff at a retail store, 40 at a manufacturing facility, or 150 across multiple locations. The platform scales from SME to enterprise without changes to onboarding or cost.

3. Does my company need a formal HRMS to use Jify?

No. Jify integrates with HRMS platforms including Keka, Greytip, Darwinbox, and ZingHR, but also supports offline integration for companies running payroll manually or via spreadsheets. A simple upload of attendance and salary data is enough to get started.

4. Will offering EWA affect my business’s working capital?

No. When an employee accesses earned wages via Jify, the company’s RBI-registered NBFC financing partners fund the transfer directly, the employer advances no cash mid-month. At the end of the salary cycle, accessed amounts are deducted from payslips as part of the normal payroll run and settled with Jify.

5. How long does it take to set up Jify?

Most companies go live within 1–3 working days. Jify assigns a dedicated onboarding team to guide setup, from data sharing to employee activation. Companies with standard HRMS integrations typically move faster; offline setups need only a data file. A 24/7 helpline is available throughout.

6. What is the ROI of EWA for a small Indian business?

The direct ROI is straightforward, since the employer cost is zero. The indirect value comes from potential reductions in attrition and recruitment costs, which vary by sector and company. Treat any specific rupee-saving figure as an estimate to be modelled against your own attrition rate and replacement costs, not a guaranteed outcome.

7. Will employees misuse EWA and spend irresponsibly?

Jify includes built-in guardrails against misuse. Withdrawal limits are set by the employer’s rule engine, typically a percentage of accrued wages per cycle, capped by tenure, grade, or department, so employees can’t access more than they’ve genuinely earned. In-app financial wellness nudges support responsible use.

*Disclaimer:

The information contained herein is not intended to be a source of advice concerning the material presented, and the information contained in this article does not constitute investment advice. The ideas presented in the article should not be used without first assessing your financial situation or without consulting a financial professional.