It is the 20th of the month, and Priya’s mother suddenly needs unexpected hospitalization. The hospital demands ₹12,000 immediately, but her next salary won’t arrive until the 1st. Like millions of salaried Indian employees, Priya faces the burden of figuring out the best way forward to meet this urgent monetary need of hers. And like most individuals, borrowing money is not an option she wishes to avail, so where does it leave her?

She could apply for a personal loan, or she has a card she could swipe the needed amount on. Here she also has another choice: her company has partnered with an Earned Wage Access (EWA) provider, so she can also stream her earned salary in her account at a minimal cost.

But how is she supposed to choose?

When looking for the cheapest emergency loan Indian salaried professionals can access, analyzing a personal loan vs credit card or exploring a credit card loan vs personal loan becomes a high-stakes calculation. Choosing the wrong option can turn a minor cash crunch into a multi-month debt trap. This article pulls back the curtain on the real numbers, hidden charges, and long-term impacts to show you exactly which choice costs you the least!

What Counts as a Cash Emergency for a Salaried Employee?

A cash emergency is any sudden, unavoidable expense that hits mid-month and cannot wait until your next payday without causing severe financial or personal harm. If you choose the wrong way to borrow, you could accidentally make your financial trouble much worse by adding 30% to 48% in yearly interest to your bill.

For salaried individuals earning between ₹20,000 and ₹80,000 a month, unexpected expenses strip away financial peace of mind instantly. In India, these cash emergencies typically fall into six distinct categories:

- Medical Emergencies: Sudden hospitalization, diagnostic tests, or critical pharmacy bills for you or your family.

- Rent Shortfalls: Facing an uncompromising landlord on the 1st when mid-month expenses cleared your account.

- School or College Fee Deadlines: Strict institutional timelines for your child’s education that carry heavy late penalties.

- Utility Disconnection Notice: Urgent electricity, water, or internet bills that risk disconnection if unpaid.

- Travel for Family Emergencies: Last-minute train or flight bookings to visit an ailing relative or a wedding in your hometown.

- Essential Appliance or Vehicle Repairs: Fixing a broken refrigerator or repairing the two-wheeler you ride to work every day.

When an emergency like a ₹15,000 rent gap hits, you don’t just need funds; you need them fast and cheap. If you use credit cards or loans without checking the fees, a quick emergency can easily turn into long-term debt.

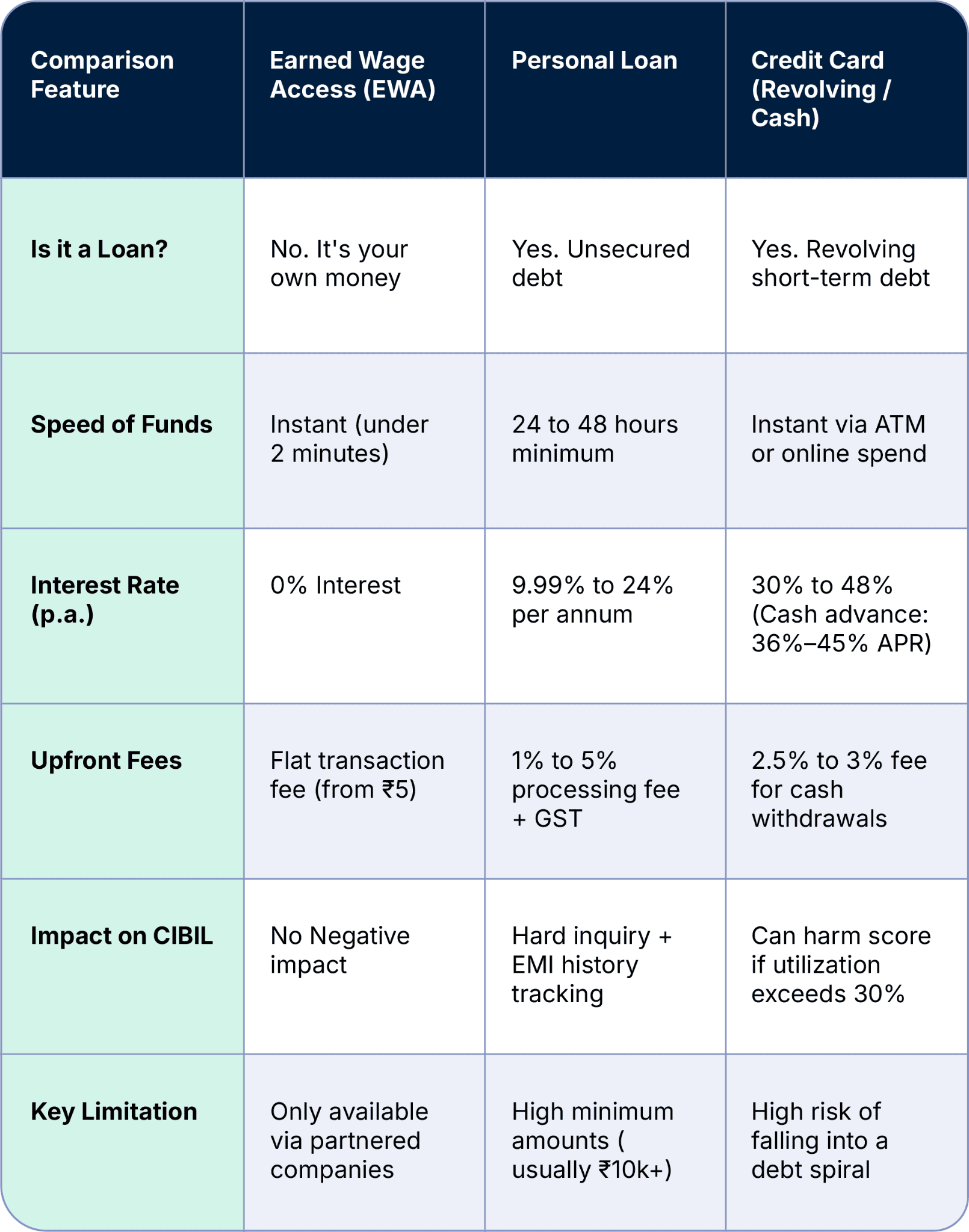

How Each Option Works

Earned Wage Access (EWA) lets you instantly withdraw your already earned salary before payday without borrowing. Personal loans provide a structured lump-sum bank loan repaid via fixed monthly EMIs. Credit cards are interest-free only if you pay off the balance in full each month.

1. Earned Wage Access (EWA)

EWA, also known as early salary access/ on-demand salary, is not a loan. It is a financial wellness tool that allows you to log into an app like Jify and withdraw a percentage of the salary you have already worked for during the month. If you require cash on the 20th, you simply access the funds you earned between the 1st and the 20th. There are no interest rates, no credit bureau checks, and the advanced amount is smoothly integrated with your regular monthly payroll cycle. EWA is only available at Jify-partnered companies.

2. Personal Loans

A personal loan is an unsecured financing option offered by banks and NBFCs. You apply, undergo complete verification, and receive a lump sum directly into your bank account if approved. You then repay this money over a fixed tenure (typically 12 to 60 months) through Equated Monthly Installments (EMIs) that carry fixed interest charges. While highly flexible, the application process requires extensive documentation and approval takes anywhere from a few hours to several days.

3. Credit Cards & Credit Card Loans

A credit card gives you a monthly revolving line of credit up to a designated limit. If you use it to swipe for an emergency and pay the entire bill by the due date, it costs you nothing. However, if you carry the balance forward or take a cash withdrawal from an ATM, it triggers massive interest compounding daily. Alternatively, some banks offer a credit card loan: a pre-approved loan that converts your available credit limit into an instant cash transfer to your bank account, bypassing long documentation but retaining high interest rates.

EWA vs Personal Loan vs Credit Card – A Three-Way Comparison

Selecting between these options depends entirely on your emergency size and your immediate capacity to repay. For minor mid-month shortfalls, EWA and credit cards offer unmatched speed, whereas structured personal loans are engineered for large-scale, long-term financial commitments exceeding ₹50,000, making a direct comparison essential to protect your wallet.

Comparing EWA and a personal loan shows a big difference: EWA operates outside the credit system , making it highly affordable, but you can only withdraw what you have earned so far that month. On the flip side, comparing a personal loan to a credit card loan highlights a different trade-off: credit card loans offer instant cash but charge very high interest for that convenience , while standard personal loans take longer to get but save you money on larger amounts.

For small emergencies under ₹10,000, your only real choices are EWA or a credit card (if you pay it off completely next month), because banks rarely give out tiny personal loans. If you need between ₹10,000 and ₹50,000, EWA is still your cheapest bet by far, with a pre-approved personal loan as a backup. For big crises over ₹50,000, a regular personal loan is the safest choice to split your payments over a long period.

💡 Midway Check-In: Your employer may already offer Jify—check if you can access your earned salary at 0% interest today to skip the borrowing cycle entirely!

The Real Cost by Emergency Size – Working Examples

The true cost of an emergency depends heavily on the interest framework and upfront fees of your chosen tool. For instance, a short-term ₹15,000 emergency can cost a mere ₹50-₹100 with EWA, whereas credit card revolving interest compounding monthly or structured personal loan processing fees can instantly multiply that cost by hundreds of rupees.

Disclaimer: The mathematical examples provided below represent indicative and approximate calculations based on average market rates in 2026. Actual costs may vary based on individual lender terms, credit scores, and employer agreements.

Scenario 1: The Minor Repair (₹5,000 Needed for 15 Days)

Ankit faces a sudden home appliance failure mid-month and needs ₹5,000 immediately.

- Via an EWA Provider: He incurs a flat, transparent transaction fee of approximately ₹5 to ₹50. Total interest cost: ₹0.

- Via Credit Card: If he fails to pay it off completely on the next bill, interest accrues at roughly 3.5% monthly. Total cost: ~₹88.

- Via Personal Loan: Most banks will not disburse a loan this small. If an app does, a minimum 3% processing fee (₹150) plus interest makes it highly impractical.

Scenario 2: The Sudden Rent Gap (₹15,000 Needed for 30 Days)

Ravi needs ₹15,000 to cover a rent shortfall until his regular payday arrives.

- Via an EWA Provider: Ravi pays an indicative flat transaction fee of ₹50 to ₹100. The funds are deducted seamlessly from his paycheck, costing him nothing further.

- Via Personal Loan: Assuming a 15% annual interest rate, he must pay an upfront processing fee of 2% (₹300) plus initial interest. Total cost: ₹300 to ₹600.

- Via Credit Card: Rolling this balance over at a 42% annual rate (3.5% monthly) creates immediate financing charges. Total cost: ₹525+ for the very first month, compounding continuously until cleared.

Scenario 3: The Medical Emergency (₹50,000 Needed for 12 Months)

Meera faces an unexpected family medical bill that requires structured long-term repayment.

- Via an EWA Provider: Not applicable. EWA is limited by your monthly earned salary and cannot provide multi-month long-term funding.

- Via Credit Card (Converted to EMI): Evaluating personal loan vs credit card emi rates shows that card EMIs hover around 16%–22% interest plus processing fees. Total interest cost over 12 months: ~₹4,500 to ₹6,200.

- Via Personal Loan: A dedicated personal loan at a competitive 12% interest rate with a 2% processing fee (₹1,000) structured over a year offers predictable repayments. Total cost: ~₹4,305 (comprising ~₹3,305 interest + ₹1,000 processing fee).

The Minimum Due Trap: Why Paying the Minimum Is a Debt Spiral

Many credit card users believe that paying the “Minimum Amount Due” (usually 5% of the total balance) keeps their account healthy and safe during an emergency. This is an expensive misconception.

If you carry a ₹15,000 emergency balance on a card charging 3.5% monthly interest (42% per annum) and pay only the ₹750 minimum due every month, your payments barely scratch the principal balance. The interest compounds relentlessly on the remaining balance day after day.

After 12 months of diligent monthly payments, you will have paid out roughly ₹9,000 in cash, yet your outstanding statement balance will still sit at over ₹14,000. The minimum due feature is deliberately engineered by credit card issuers to keep borrowers paying indefinitely while keeping them locked into a cycle of high-interest debt.

Hidden Costs Most People Miss

Financial products frequently mask their true expense behind secondary charges that are hidden deep within the fine print. While personal loans carry mandatory upfront processing fees and strict foreclosure penalties, credit cards penalize users with steep over-limit charges, late fees, and heavy interest charges applied to your full balance instead of just the leftover amount.

Personal Loan Hidden Costs

- Upfront Processing Fees: Lenders typically deduct 1% to 5% of your approved loan amount right at the start. If you are approved for ₹50,000, you might only see ₹48,000 land in your account, even though you owe interest on the full ₹50,000.

- GST on Financial Services: A mandatory 18% Goods and Services Tax (GST) is levied on top of your processing fees and bank documentation charges.

- Foreclosure and Prepayment Penalties: If you come into extra cash and want to clear your personal loan before the tenure ends, banks often charge an extra 2% to 5% fee on the remaining principal.

- EMI Bounce Charges: If an automated National Automated Clearing House (NACH) debit fails due to insufficient funds, you will face cross-bank bounce charges ranging from ₹300 to ₹500 per instance.

Credit Card Hidden Costs

- Retroactive Interest: If you pay off 95% of your bill and leave just ₹500 unpaid, the bank charges 30%–48% interest on your entire bill from the exact day you made those purchases, not just on the leftover ₹500.

- The Cash Advance Premium: Taking cash out of an ATM with a credit card costs an immediate fee of 2.5% to 3%. Even worse, you don’t get an interest-free period. Interest starts building up the exact day you withdraw the money, pushing the yearly rate up to 36%–45%.

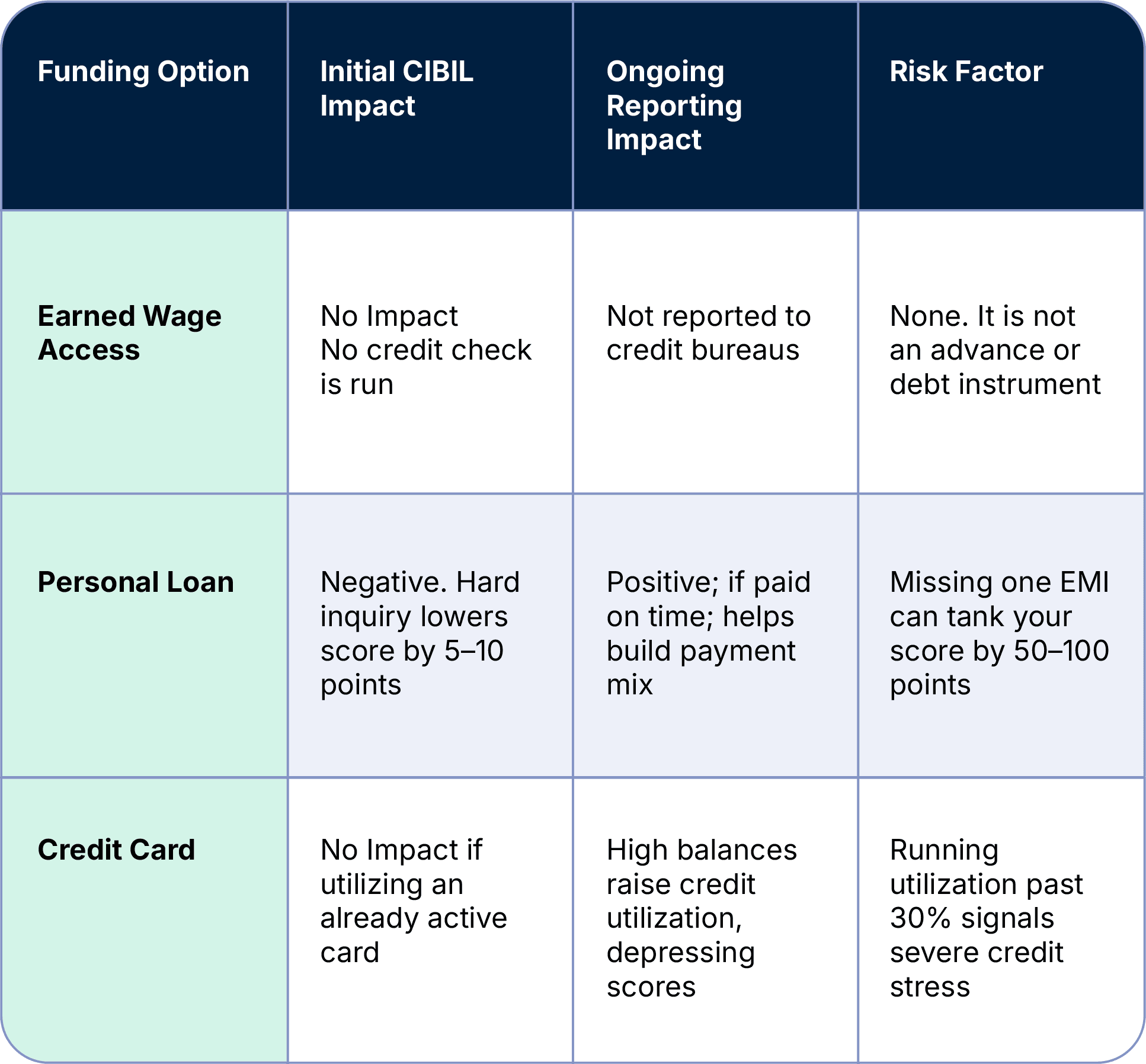

How Each Option Affects Your CIBIL Score

Your choice of emergency funding leaves an immediate footprint on your CIBIL score through different reporting mechanisms. While Earned Wage Access features a zero-impact design because it uses your own money, personal loans trigger hard credit inquiries, and credit cards can heavily damage your rating if your credit utilization ratio crosses the critical 30% threshold.

Every single formal personal loan application triggers a “hard inquiry,” telling credit bureaus you are actively hunting for debt. If you apply to multiple lenders quickly during an emergency, your score drops rapidly. Conversely, while credit cards skip the inquiry step, running up a high balance relative to your credit ceiling spikes your credit utilization ratio india metrics. Crossing the 30% utilization threshold hurts your CIBIL rating, even if you make your minimum payments on time every single month.

When NOT to Use a Credit Card or Personal Loan

Avoid using a credit card if you need physical cash or cannot clear the full bill next month. Skip a personal loan if your requirement is under ₹10,000 or your CIBIL score is below 700. In these specific scenarios, both traditional options stop being helpful tools and instead become expensive financial traps.

When you are staring at an urgent hospital bill or an unyielding landlord, your natural instinct is to grab the first financial tool within reach. You might have a credit card sitting in your wallet, or a flashy “pre-approved loan” notification blinking on your phone.

It feels like an instant lifesaver, but borrowing under panic can blind you to serious warning signs. Some financial tools are simply not built for certain types of emergencies. Before you swipe your card or click “apply” on a loan, you need to check for the major red flags that mean an option will do your wallet more harm than good.

Do NOT Use a Credit Card If:

- You cannot pay the full bill next month: If you carry the emergency balance over, a 30%–48% annual interest rate kicks in immediately.

- You need actual physical cash: Withdrawing cash from an ATM triggers immediate 2.5%–3% upfront fees and 36%–45% APR interest from day one.

- Your credit utilization is already above 30%: Maxing out your card further will trigger a sharp drop in your CIBIL score.

Do NOT Apply for a Personal Loan If:

- You need less than ₹10,000: Upfront processing fees (1%–5%) and GST make borrowing tiny amounts through a formal loan highly expensive.

- You need the money this very hour: Traditional bank verifications and processing timelines usually take 24 to 48 hours minimum.

- Your CIBIL score is below 700: You risk getting your application rejected outright, which damages your credit report, or being forced into punishingly high interest rates.

Conclusion

For salaried employees, EWA is the most overlooked yet most affordable emergency option for mid-month cash gaps. For larger amounts or when EWA isn’t available, a pre-approved personal loan is far cheaper than carrying a credit card balance. The credit card is only “free” if you pay the full bill.

Take Control of Your Paycheck Today

- Your employer may already offer Jify: Check if you can access your earned salary at 0% interest today.

- Ask your HR team to set up Jify: Setup takes under 48 hours and comes at zero cost to the company.

- Download the Jify app: Once your company is live with Jify, just download the app and access your earned salary instantly, any time, anywhere!

FAQs:

Q1: Is EWA cheaper than a personal loan?

A: Yes, for most mid-month emergencies. EWA through Jify is interest-free — you only pay a flat transaction fee starting from ₹5. A personal loan charges 9.99%–24% per annum plus a processing fee of 1%–5% of the loan amount. For a ₹15,000 emergency repaid in 30 days, EWA costs under ₹100 while the same personal loan can cost ₹300–₹600, including processing fee and first-month interest. EWA is only available at Jify-partnered companies.

Q2: Is it better to use a credit card or a personal loan for an emergency?

A: It depends on two things: the size of the emergency and whether you can pay the full credit card bill next month. For amounts under ₹25,000 where you can repay in full by the next due date, a credit card costs you nothing. If you cannot repay in full, a personal loan is significantly cheaper — 10%–24% p.a. vs 30%–48% p.a. on revolving credit card interest. Never use a credit card cash advance for emergencies — it starts charging interest from day one.

Q3: Does taking a personal loan affect my CIBIL score?

A: Yes, in two ways. When you apply, the lender does a hard credit inquiry, which typically drops your CIBIL score by 5–10 points temporarily. However, if you repay all EMIs on time, your score usually recovers and improves over 12–18 months. Missing even one EMI can cause a 50–100 point drop. EWA has zero impact on your CIBIL score because it is not classified as a loan and is not reported to credit bureaus.

Q4: What is the actual interest rate on a credit card in India in 2026?

A: Most Indian credit cards charge 30%–48% per annum (approximately 2.5%–4% per month) on outstanding balances. This applies from the transaction date if you carry any balance forward — there is no grace period on the carried amount. A cash advance (ATM withdrawal) is even more expensive: an immediate fee of 2.5%–3% plus the same monthly interest starting from day one, with no grace period. Effective APR on cash advances is typically 36%–45%.

Q5: What are the hidden charges on a personal loan in India?

A: The most common hidden costs are: (1) Processing fee of 1%–5% of loan amount, deducted upfront from the disbursed amount — so you receive less than approved; (2) GST at 18% on the processing fee; (3) Prepayment or foreclosure charges of 2%–5% if you repay early; (4) EMI bounce charges of ₹300–₹500 if the auto-debit fails; (5) Penal interest on overdue EMIs. Always ask for the total cost of borrowing (TCB) — not just the interest rate.

Q6: What is the cheapest way to borrow ₹10,000 urgently in India?

A: If your company is Jify-partnered, use EWA — interest-free, instant, flat fee of ₹5–₹100. If you have a credit card and can repay the full amount by the next due date, use it for free. If neither applies, a pre-approved personal loan from your salary account bank is the fastest (same-day disbursement possible). Most banks have minimum loan amounts of ₹10,000–₹50,000, so ₹10,000 may be near the minimum. Avoid credit card cash advances — the most expensive short-term option.

Q7: Does using a credit card for emergencies hurt your credit score?

A: It depends on how you use it. Using a credit card for emergencies and paying the full bill on time is fine — it actually builds your credit history. The problems arise when: (1) You use more than 30% of your credit limit, which signals credit stress to CIBIL scoring models even if you pay on time; (2) You only pay the minimum due while carrying a balance, leading to rising utilization; (3) You take a cash advance, which is flagged as a negative indicator. Keeping utilization below 30% is the key rule.

*Disclaimer:

The information contained herein is not intended to be a source of advice concerning the material presented, and the information contained in this article does not constitute investment advice. The ideas presented in the article should not be used without first assessing your financial situation or without consulting a financial professional.