With the onset of flexible work options lately, smartphones, laptops, tablets, and even wearables aren’t luxuries, they’re necessities. Whether you’re attending virtual meetings, collaborating on cloud documents, or managing work-life balance through productivity apps, your devices directly impact your career performance and earning potential.

Yet most employees face a crucial financial decision, i.e., should they opt for device leasing or buying? Understanding the difference between lease vs buy devices, including options for cash purchases, EMI financing, or salary deduction device leasing programs, can save you thousands and give you access to better technology sooner.

What Is Device Leasing for Employees?

Employee device leasing is an arrangement where your company, through a partnering leasing provider, allows you to use a premium device for a fixed period while you pay a monthly rental instead of bearing the full cost upfront.

Under this model, the ownership of the device, whether it’s a smartphone, laptop, or tablet, remains with the leasing company or your employer throughout the lease term. Once the term ends, typically after 12 to 36 months, you have several options. You can return the device and upgrade to a newer model, continue using it by extending the lease, or, in some cases, purchase it at a predetermined buyout price.

What makes this particularly convenient for employees is the salary deduction device leasing structure. The monthly rental is automatically deducted from your payroll as a fixed amount, eliminating the need for manual payments or tracking due dates. This seamless integration with your salary makes budgeting predictable and ensures you never miss a payment, while giving you access to devices that might otherwise be beyond your immediate purchasing power.

How Does Employee Device Leasing Actually Work?

The process is straightforward and designed for convenience:

The Simple 5-Step Process:

- Browse a curated catalogue of devices offered through your employer’s leasing program and select the smartphone, laptop, or tablet you need

- Sign up through your company’s designated leasing partner, completing a simple enrollment process

- Receive your device once approved

- Pay a fixed monthly rental, deducted directly from your salary

- At lease term end, return it for an upgrade, extend the lease, or exercise a buyout option if available

What’s typically included:

- Manufacturer warranty coverage

- Regular service support

- Sometimes accidental damage protection (specifics vary by provider, so always check your program’s terms)

Key advantages of salary-linked payments:

- Everything happens automatically through the salary deduction device leasing

- No need to remember due dates or manage separate EMI accounts

- Monthly rentals break down a ₹60,000-80,000 shock into manageable ₹2,000-3,000 payments, making premium devices accessible without disrupting your budget

Important Considerations:

- If you leave the company mid-lease, you may need to clear outstanding dues or transfer the lease

- Loss or damage policies differ across programs. Understand your specific terms upfront

What Does Buying a Device Mean (Cash or EMI)?

Buying a device means you pay the full price either immediately or over time. The device becomes your personal property from day one.

There are two primary ways to buy:

1) Upfront purchase

You pay the entire amount using your savings, debit card, or credit card. The device is yours instantly with no future payment obligations, though it requires significant liquid cash often ₹50,000 to ₹1,00,000 for premium devices.

2) EMI (Equated Monthly Instalments)

You finance the purchase through a bank, NBFC (non-banking financial company), or credit card provider, spreading payments over 3 to 24 months. While this eases the immediate burden, you pay interest rates ranging from 12% to 18% annually, plus potential processing fees. These EMIs become another fixed monthly commitment alongside your other expenses.

As the owner, you enjoy complete freedom customise, modify, or sell the device whenever you want. However, you’re also solely responsible for all repairs, maintenance costs, insurance, and eventual upgrades. When technology advances or your device ages, the cost and hassle of replacement fall entirely on you.

How Does Buying a Device Affect Your Monthly Budget?

An upfront purchase immediately depletes your savings or emergency fund. Spending ₹70,000 on a laptop means that money is no longer available for medical emergencies, unexpected expenses, or planned goals for several months until you rebuild your reserves.

Choosing EMI adds another fixed commitment to existing monthly obligations

Consider a typical employee’s income split:

- 30% for rent

- 20-25% for existing EMIs (education loan, bike loan, credit cards)

- 25-30% for living expenses

- Ideally, 20% for savings

A new ₹4,000 device EMI squeezes into this already tight equation. Often forces you to either reduce savings or compromise on lifestyle

The Long-Term Ownership Math:

If you keep the device for four to five years, the per-month cost does decrease over time. Example: A ₹60,000 laptop used for five years effectively costs ₹1,000 monthly

However, this only works if the device remains functional and meets your needs throughout that period

The Real Financial Caution:

Buying high-end devices on EMI without proper planning can derail financial goals

That ₹5,000 monthly phone EMI could instead be:

- Your travel fund

- Emergency corpus contribution

- Investment amount for wealth building

These goals get delayed by 12-18 months while you’re locked into payments

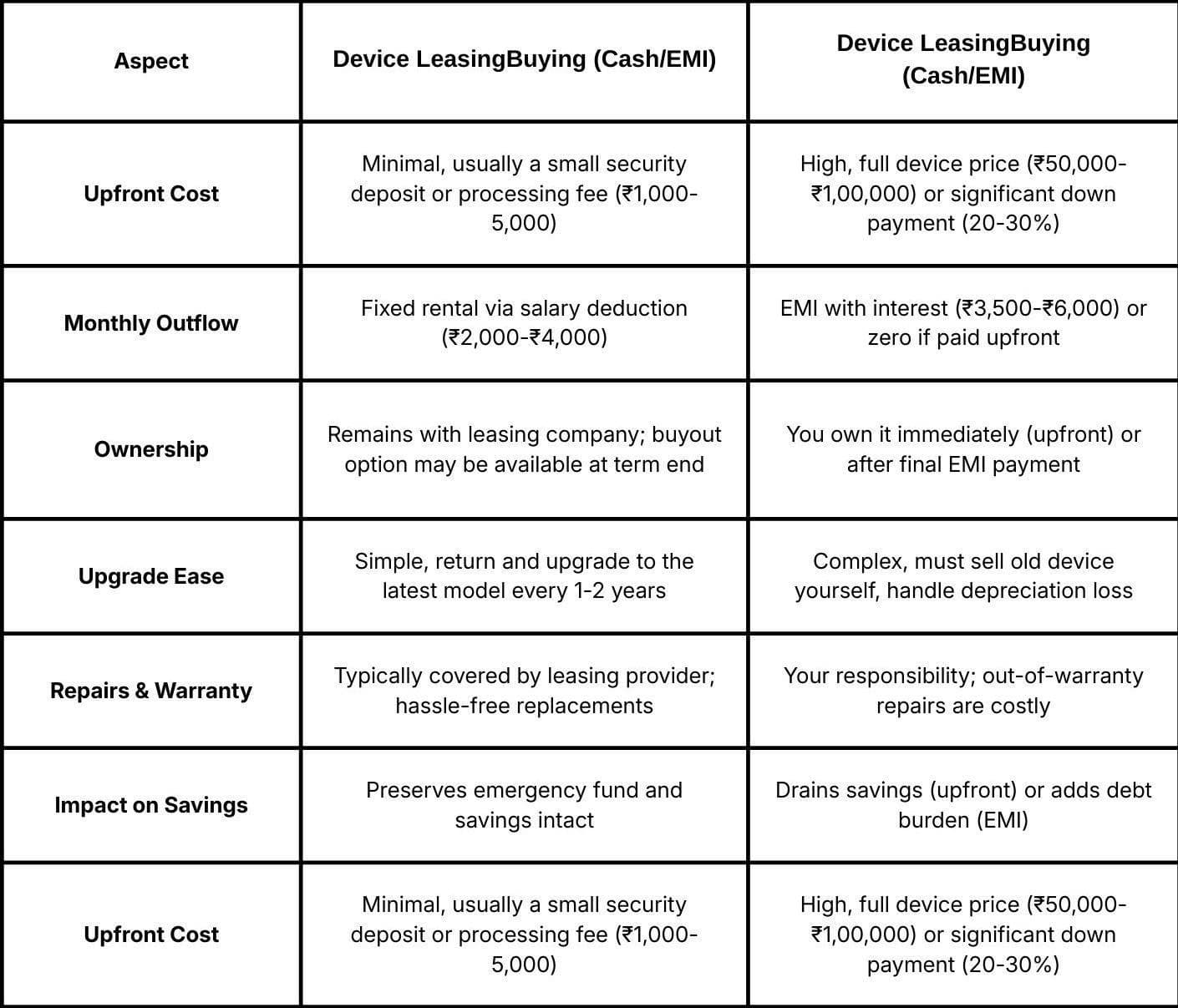

Device Leasing vs Buying: Key Differences at a Glance

There’s no universally ‘perfect’ choice between lease vs buy devices, the right decision depends on your cash flow situation, how long you typically keep devices before upgrading, and whether you value ownership or prefer flexibility and hassle-free maintenance.

Here’s a side-by-side comparison to help you evaluate:

When Does Device Leasing Make More Sense for Employees?

Employee device leasing becomes the smarter choice in several specific situations:

- You’re a tech enthusiast who upgrades frequently: If you prefer having the latest iPhone or MacBook every two years, leasing eliminates the hassle of selling depreciated devices on resale platforms. You simply return and upgrade without dealing with buyers, negotiations, or value loss.

- You want to protect your savings: When your emergency fund is still building or you’re saving for major goals like a home down payment or wedding, salary deduction device leasing lets you access premium devices without touching those critical reserves.

- You value predictable budgeting: Fixed monthly rentals automatically deducted from salary mean no surprises, no missed payments, and no credit score risks, unlike managing multiple EMI accounts across different lenders.

- Your device is primarily a work tool: If you need a reliable laptop or phone for professional productivity rather than personal ownership pride, leasing offers functionality without the emotional or financial attachment.

- You avoid maintenance headaches: When the warranty expires or screens crack, leasing programs typically handle repairs and replacements, saving you time and unexpected repair costs.

A Simple Framework to Decide: Lease or Buy Your Next Device?

Use this practical checklist to evaluate what works best for your situation:

1. Monthly Budget Reality Check: After accounting for rent, existing EMIs, groceries, and essentials, how much can you comfortably allocate toward devices without stress? If it’s under ₹3,000, leasing might offer better devices than what EMI budgets allow.

2. Upgrade Frequency Pattern: Honestly assess your history. Do you typically upgrade every 2-3 years to stay current, or do you use devices for 5+ years until they’re completely obsolete? Frequent upgraders benefit more from leasing’s flexibility.

3. Savings Impact Assessment: Would spending ₹60,000-₹80,000 upfront significantly deplete your emergency fund (ideally 6 months’ expenses) or derail important financial goals? If yes, preserve your savings and consider leasing.

4. Employer Program Availability: Does your company offer corporate device leasing with salary deduction? This infrastructure makes leasing seamless and often includes better terms than consumer financing.

5. Ownership vs. Access Mindset: Be honest, do you emotionally value owning your gadgets, or do you primarily care about having reliable, functional devices for work and life?

6. Maintenance Comfort Level: Are you willing to handle repairs, insurance, and troubleshooting yourself, or do you prefer hassle-free support included in your monthly payment?

7. Credit and Debt Load: Are you already managing multiple EMIs? Adding another might strain your debt-to-income ratio and credit score.

A Simple Framework to Decide: Lease or Buy Your Next Device?

Use this practical checklist to evaluate what works best for your situation:

1. Monthly Budget Reality Check: After accounting for rent, existing EMIs, groceries, and essentials, how much can you comfortably allocate toward devices without stress? If it’s under ₹3,000, leasing might offer better devices than what EMI budgets allow.

2. Upgrade Frequency Pattern: Honestly assess your history, do you typically upgrade every 2-3 years to stay current, or do you use devices for 5+ years until they’re completely obsolete? Frequent upgraders benefit more from leasing’s flexibility.

3. Savings Impact Assessment: Would spending ₹60,000-₹80,000 upfront significantly deplete your emergency fund (ideally 6 months’ expenses) or derail important financial goals? If yes, preserve your savings and consider leasing.

4. Employer Program Availability: Does your company offer corporate device leasing with salary deduction? This infrastructure makes leasing seamless and often includes better terms than consumer financing.

5. Ownership vs. Access Mindset: Introspect if you emotionally value owning your gadgets, or do you primarily care about having reliable, functional devices for work and life?

6. Maintenance Comfort Level: Are you willing to handle repairs, insurance, and troubleshooting yourself, or do you prefer hassle-free support included in your monthly payment?

7. Credit and Debt Load: Are you already managing multiple EMIs? Adding another might strain your debt-to-income ratio and credit score.

How Jify’s Device Leasing Fits Into Your Financial Life

Jify’s employee device leasing program is designed to align with how you actually earn and spend. Through a simple salary-linked structure, you choose from a curated catalog of quality smartphones, laptops, and tablets, then pay manageable monthly rentals that are automatically deducted from your payroll; no separate loan applications, credit checks, or payment tracking required.

For your wallet, this means zero large upfront costs that drain savings. Instead of parting with ₹70,000 immediately or adding high-interest EMIs to your debt load, you pay predictable monthly amounts (typically ₹2,000-₹4,000) that fit seamlessly into your budget, leaving room for investments, travel, or building your emergency fund.

For your peace of mind, Jify eliminates the upgrade hassle. Forget negotiating with buyers on resale apps or dealing with device depreciation. When your lease term ends, simply return and upgrade to the latest model. Maintenance and warranty coverage (where included) mean unexpected repair bills won’t derail your monthly budget.

Conclusion: The “Right” Choice Is the One That Protects Your Future Self

Whether you choose the flexibility of salary deduction device leasing or the ownership of buying outright, the best decision is one that doesn’t compromise your emergency fund or delay important life milestones.

Your smartphone or laptop should enhance your career and productivity, not become a source of financial stress or regret six months down the line. Before making your next device decision, take time to honestly assess your cash flow, upgrade patterns, and financial priorities.

Ready to make smarter device decisions? Explore Jify’s employee device leasing options and discover how predictable monthly rentals can give you access to premium technology while protecting your savings and long-term financial wellness. Your future self will thank you for choosing wisely today.

*Disclaimer:

The information contained herein is not intended to be a source of advice concerning the material presented, and the information contained in this article does not constitute financial advice. The ideas presented in the article should not be used without first assessing your financial situation or without consulting a financial professional.